My approach to Equity Valuation

My preferred approach is to base valuation on insights gained from the Return on Capital Employed (ROCE) framework. I feel that the ROCE framework is an excellent framework to understand the competitive position of a firm, and to further break up ROCE into Capital productivity and Operating Margin. A capital productivity productivity of 3X, and an Operating margin of 7% are good thresholds to identify an investment candidate. Firms whose figures are much higher than these values will be rewarded with much higher valuation multiples.

As a next step in the valuation process, I look at current EPS and use a 12x-13x multiple to produce a first valuation per share. This multiple can increase upto 30x based on the superior ROCE metrics. In this way, you are paying for future growth but based on the economic moat of the firm in question, and for how long it can sustain its earnings from competition. Importantly, we are not basing this on the guidance from analysts or the firm in question.

As the risk free rate decreases, the multiple will increase, but I do not wish to incorporate this into my valuation approach because as the risk free rate increases or decreases, the value of my firm can increase or decrease based on factors external to the firm. This produces too much risk as compared to my preferred approach to investing. This is my margin of safety, but also means that investment opportunities are harder to come by and few and far in between.

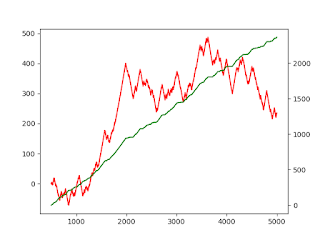

Authoritative illustration here: http://people.stern.nyu.edu/adamodar/pdfiles/val3ed/c18.pdf. A key chart from the above illustration, reproduced below.

pedata.xls: This dataset on the Web summarizes price earnings ratios and fundamentals by industry group in the United States for the most recent year

Comments

Post a Comment